piranka

When I last covered Applied Blockchain (NASDAQ:APLD) for Seeking Alpha, my main argument for calling it a hold was how overvalued it was compared to both data center peers and Bitcoin (BTC-USD) mining peers. Since that article, the price of the stock has doubled and the valuation metrics have actually improved. In this follow-up, we’ll go over a few things that have changed in the three months since my last article, revisit some of the valuation metrics that we explored in mid-June, and try to assess the health of Bitcoin miners broadly.

What’s new?

Since June, the company has made a few significant non-earnings related announcements. The first was that the company has entered an agreement with Marathon Digital (MARA) for hosting services. While the agreement will see Marathon relying on Applied Blockchain for 90 megawatts of hosting capacity at APLD’s Texas facility and 110 megawatts out of North Dakota, the hosting capacity could ultimately reach a total of 270 megawatts by mid-2023. As the rollout of Marathon’s hosting won’t commence until Q422, this will be incremental revenue for APLD in upcoming quarterly filings. The Marathon news no doubt helped the share price of APLD immediately.

Something else that has impacted the share price dynamics is the cancelling of approximately 5% of APLD shares outstanding. The shares were held by Sparkpool. Sparkpool, one of the anchor customers from Applied Digital’s May investor deck, has discontinued operations. From Page 56 of APLD’s annual report:

SparkPool ceased providing the contracted services for the Company, and agreed to forfeit shares to compensate for future services that will not be rendered. As a result of this agreement, 4,965,432 shares of Common Stock were forfeited and canceled by the Company, reducing the number of shares of Common Stock outstanding.

It’s never good seeing a customer cease operations, and we’ll explore the possibility of this continuing later in the article. First, another fairly large news item the company announced recently is a proposed name change from “Applied Blockchain” to “Applied Digital” that will be voted on by shareholders in November. From the company:

While Applied Blockchain continues to be a premier provider of digital infrastructure for many cryptocurrency mining operations, it is important for the Company to distinguish that its next-generation datacenters support many other high-performance compute applications

I share this view. If approved, the name change is not a move that will impact the company’s bottom line immediately. But I do view it as a smart decision. In an ESG environment like the one we’re seeing from many corporate initiatives, I think subtle changes like this one could ultimately help the company diversify its customer base long term. It’s a good step toward eliminating the notion that Applied is just a crypto company and opens the door a bit more to HPC services. Finally, the company beat revenue expectations in the last quarter with $7.5 million in topline revenue against guidance of $7 million.

Valuations

In June, I chose Hut 8 Mining (HUT), Marathon Digital (MARA), and Riot Blockchain (RIOT) as Bitcoin mining peers for Applied Blockchain. At that time, APLD was trading at 37 times Price/Sales TTM and 19 times EV/Sales FWD. These figures were generally between 10 to 20 times higher than the multiples for the selected Bitcoin mining competitors. While APLD is still overvalued compared to those companies trailing twelve months, APLD’s valuation has come down considerably while the peers have largely seen multiple expansion:

| APLD | HUT | MARA | RIOT | |

| Price/Sales TTM | 14.03 | – | 6.13 | 2.53 |

| EV/Sales FWD | 1.03 | 2.58 | 11.03 | 2.51 |

| EV/Sales TTM | 21.68 | 2.16 | 10.49 | 35.29 |

Source: Seeking Alpha

Compared to the other three, APLD is now cheaper based on forward EV/Sales. But again, pure-play miners aren’t a perfect comp because Applied serves as more of a datacenter for the miners. From that perspective, the datacenter REITs that I used in the last article for multiple comparisons were Digital Realty Trust (DLR), Equinix (EQIX), and Innovative Industrial Properties (IIPR).

| APLD | DLR | EQIX | IIPR | |

| Price/Sales TTM | 14.03 | 7.52 | 8.72 | 9.03 |

| EV/Sales FWD | 1.30 | 10.84 | 9.88 | 10.02 |

| EV/Sales TTM | 21.68 | 11.29 | 10.97 | 11.07 |

Source: Seeking Alpha

Here we can see APLD is still overvalued on the trailing metrics but much cheaper on forward EV/Sales. I think it’s important to remember that even though Applied Blockchain’s business model may be closer fundamentally to that of datacenters, the company is still going to be reliant on a healthy Bitcoin mining industry for revenue. Miners are currently facing a very difficult macro situation, and I think it’s important for APLD shareholders to keep that in mind.

Miner Headwinds

We now know that APLD will have a business relationship with Marathon Digital. That’s going to help alleviate the customer concentration problem that I cited in my June article. The company has given insight into who currently makes up that customer base:

We have material customer concentration in our co-hosting business as of May 31, 2022. We have entered into contracts with JointHash Holding Limited (a subsidiary of GMR), Spring Mud, LLC (a subsidiary of GMR) Bitmain Technologies Limited, F2Pool Mining, Inc. and Hashing LLC (a subsidiary of GMR) to utilize our first co-hosting facility.

One thing to be aware of is F2Pool Mining does have an Ethereum (ETH-USD) mining footprint, though I don’t think we’ll know how much of the mining it does with Applied Digital is Ethereum-based. Ethereum miners are facing serious disruption after the merge from Proof-of-Work to Proof-of-Stake. I’ve detailed why they can’t just switch all of their GPU machines to Ethereum Classic (ETC-USD) mining here. ETH or no ETH, we know APLD has exposure to BTC miners and those entities could be facing solvency concerns fairly soon.

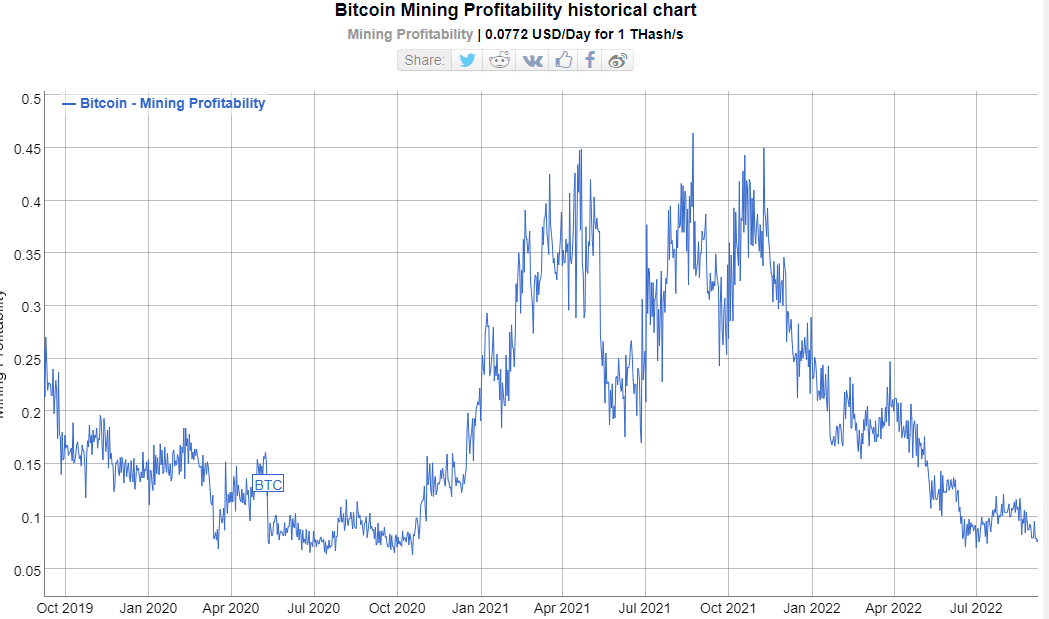

As the hashrate for Bitcoin continues to increase, the miners need the price of Bitcoin to rise to counteract the increased difficulty in attaining the block reward. Since Bitcoin isn’t increasing in price, we’re currently seeing some of the tightest broad miner margins in the last two years.

BitInfoCharts

This miner profit squeeze could ultimately lead to rigs getting turned off and mining operators defaulting on obligations. While hashrate and miner profit don’t directly harm Applied Blockchain’s revenue, if APLD’s customers can’t continue operating at lower Bitcoin prices, it has the potential to impact long-term receivables and create customer churn.

Summary

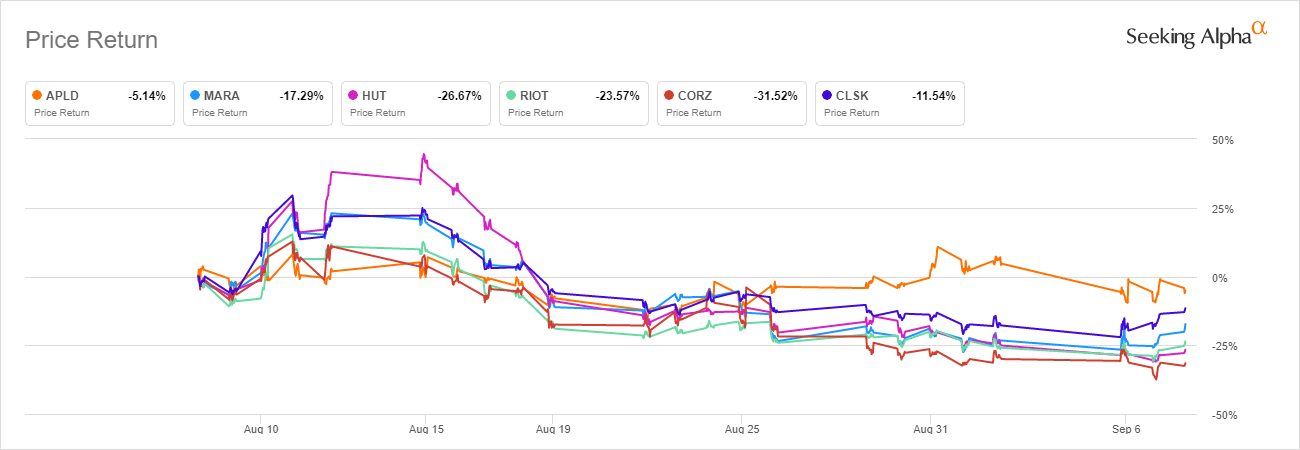

I still think Applied Blockchain is a very interesting equity for crypto business investors to consider. While the rest of the public mining peers have seen a bit more pressure on share prices over the last month, APLD has held up fairly well, having taken only a 5% haircut.

Seeking Alpha

With improved valuation metrics and a new industry-leading customer generating incremental revenue later this year, there’s a lot to like about Applied Blockchain. I don’t currently own shares because I still believe we are in more of a risk-off environment at the moment. But APLD is one I will consider going long in 2023. I want to see what, if any, impact the Ethereum merge has on APLD’s customers. And I’d like to see Bitcoin mining become more profitable than it currently is to take pressure off the industry more broadly. While I wouldn’t be selling if I was long APLD, I think it’s still a hold for now.