The world is fast progressing within the technology domain and digital services have penetrated to the unexplored corners of life. Digital transformation has become the backbone of companies and industries throughout the planet.

Traditional banking and lending which were thriving a couple of years back, are dying a quick death. Post the pandemic the banks and other financial institutions have increased the push on digital channels for acquisition and customer servicing. Agile and scalable lending platforms are cutting acquisition costs and convey in growth in loan volumes.

India’s eleven largest banks namely ICICI Bank Ltd, Axis Bank Ltd, Kotak Mahindra Bank, HDFC Bank, Yes Bank, Standard Chartered Bank, RBL Bank, South Indian Bank, etc. have come together to form a consortium for leveraging the blockchain technology.

Blockchain solutions will help increase operational efficiency, faster TAT, enhanced customer delight, increase transparency, and authenticity of transactions. Banks are going to be ready to make better credit decisions thanks to the globally shared and distributed network and increased communication between banks. Blockchain will reduce fraud and data manipulation and can deliver better portfolios.

What is Blockchain?

“Blockchain is an immutable transaction ledger database shared by all parties in a distributed network, which records and stores every transaction that occurs in the network, creating an irrevocable and auditable transaction history.”

Some of the key characteristics of a Blockchain:

- Distributed: The information is stored across multiple nodes (computers) across the network.

- Shared: The information is not owned by single party.

- Immutability: Once data is entered and verified, it cannot be tampered with. The cryptographic hash ensures immutability.

- Transparent & Secure: All records stored on the database are visible to all stakeholders and cannot be altered or modified by a single stakeholder.

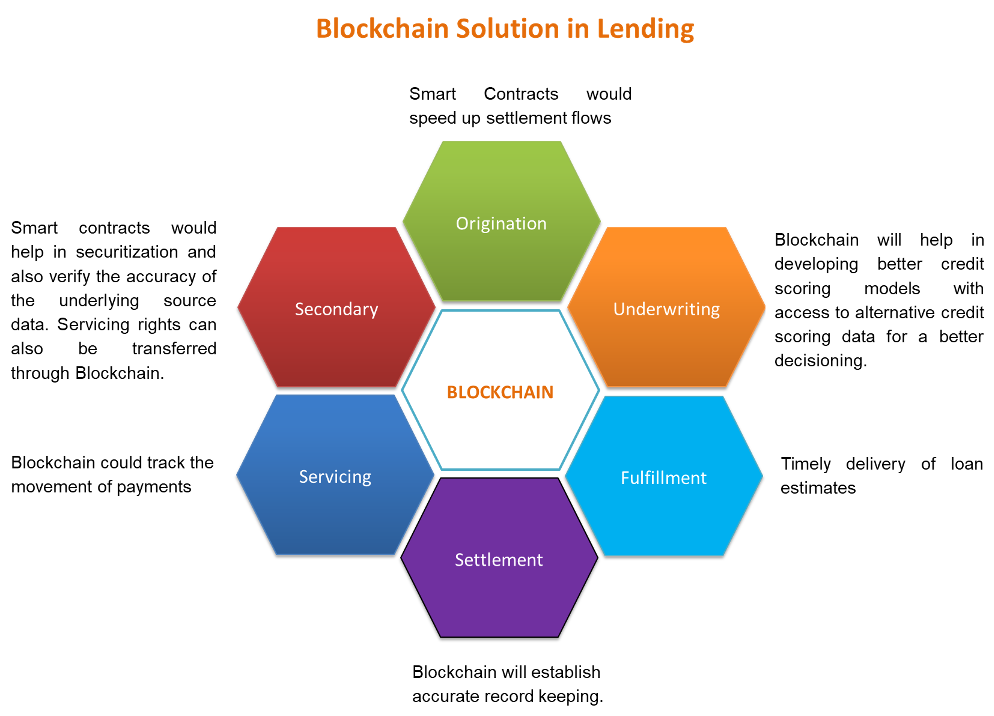

Blockchain use cases in Mortgage lending:

1. Credit Bureaus: Blockchain characterizes immutability in recording transactions and works on a shared network which eliminates the need of an intermediary. The origination of a credit record happens from a bank or a financial organization. On a Blockchain, the members are the owners and no third party (bureau) is liable for maintaining the record. whenever a member records a transaction, it’s verified by consensus of the members on the network. Once verified and updated, every other parties ledger record also gets updated. Decentralised storage eliminates the threat of hacking and data breaches and also brings down the value of access for the members. Consumers also get direct access to their credit data allowing them to access the info originating from the source.

2. Accurate Credit profile- A Blockchain network may enable the secure sharing of customer profile data across member institutions. Data like KYC, credit scores, profiling data, account types, relationship data, business profiles, structured and unstructured data, and other social media data held across multiple member institutions et al. might be combined to make a far better , secure, and accurate profiling for a credit decision. A Blockchain could also facilitate the management of customer consent across institutions. The abundance of knowledge on the network can help design better and more custom-fit solutions for the top consumers.

3. Fraud Reduction– Frauds in mortgage loans may be a massive problem for lenders. ranging from document frauds, data fudging, property ownership frauds, etc., a lender bank or financial organization has got to believe tons of unverified data during deciding. Blockchain thanks to its immutable nature eliminates any quite data manipulation once it’s verified at the origination. due to the decentralised data storage and data origination happening from multiple sources, manipulating any specific set of knowledge without the network confirming the transaction is impossible. This ensures the info integrity and trust on the network.

4. Accurate Land records: Land /property records are currently maintained in geo scatter. These records are susceptible to fraud and manipulation. The accuracy and authenticity are difficult to determine . For a financial institution/bank that’s extending a mortgage-backed loan is primarily hooked in to the authenticity of those records while extending this loan. Blockchain will help establish trust and accuracy to take care of these registry records. The Land Management System on the Blockchain would usher in transparency, accuracy, speed fraud minimization, and reduced documentation to the transactions. this is able to make it easier for banks and financial institutions to hurry up mortgage transactions and at an equivalent time eliminate the danger of fraud and manipulation.

5. Alternative credit Scoring: Blockchain are often wont to collect alternative data for a more comprehensive credit scoring model. This alternative data can include payment information of utilities, telephone payments, property ownership, social media profile, ownerships, and other qualitative information which can enrich the credit scoring models and supply a more accurate assessment. thanks to the inherent nature of being a tamper-proof technology, security, and trust in data sharing are going to be more for the consumers. the info collection are going to be an ongoing process and therefore the data will get updated on a real-time basis.

Conclusion:

Every industry today is witnessing a serious shift in the way data is collected, managed, stored and disseminated. Within the last few years we have witnessed an incredible growth in new age fintech companies who are leveraging technology to style new and efficient financial solutions. Data fraud and security are the being looked at more as niche and critical factor in managing data. Blockchain provides a more fertile ground for innovation for these fintech companies to explore “better than the best” models for the finance sector. There are many more blockchain use cases in the finance industry and as we progress on the path of innovation we will have more use for blockchain.

Author: Saroj Kumar Dash, Senior Vice president at Religare Finvest Ltd